Mispriced Infrastructure: The Hidden VC Opportunity in Parking and Storage Assets

The story unfolding around Petco Park is not fundamentally about parking. It is about pricing power, supply constraints, and the monetization of overlooked real estate assets in dense urban environments.

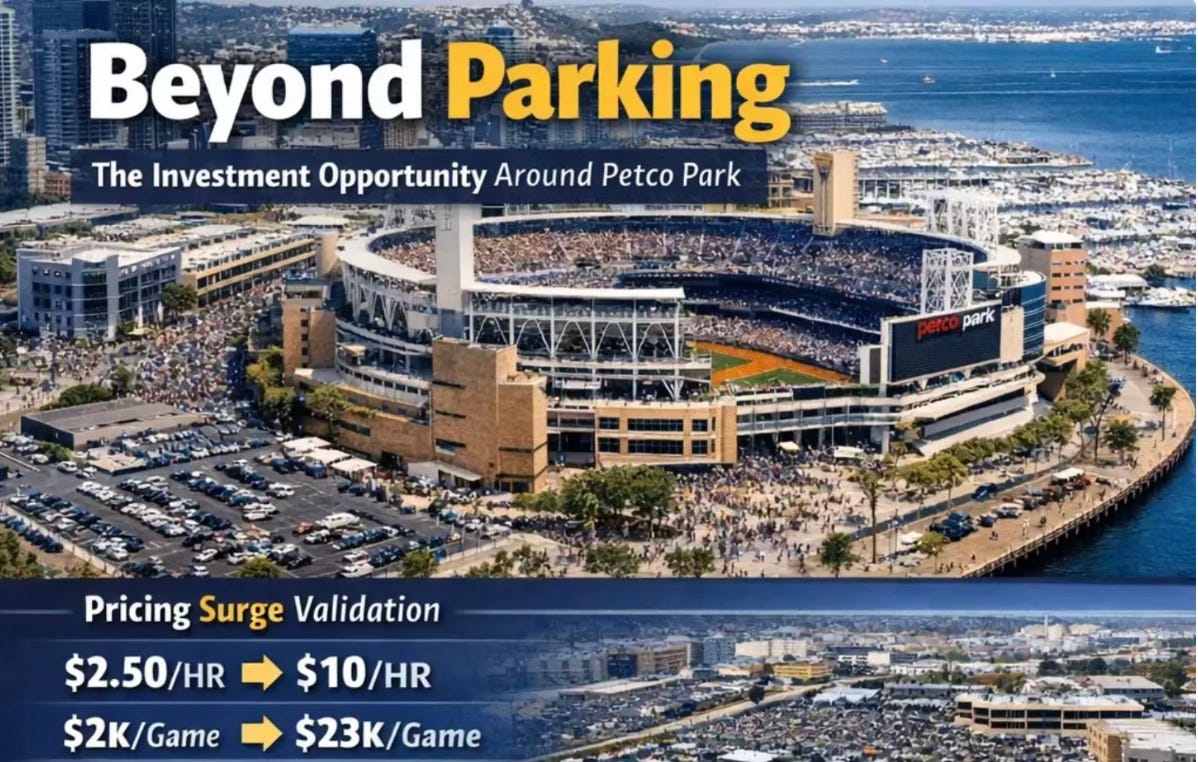

From a venture perspective, what stands out immediately is the magnitude of pricing elasticity. A shift from roughly $2.50 per hour to $10 per hour, paired with a jump from approximately $2,100 to $23,000 in per-game parking revenue, is not incremental improvement—it is a structural repricing of an asset class. The market is signaling, clearly and repeatedly, that demand for proximity, convenience, and time savings around high-density events is significantly undervalued.

This demand is not speculative. It is programmatic. With 40,000 to 50,000 attendees flowing into a single geographic node dozens of times per year, the result is a series of predictable, high-intensity demand spikes. In most sectors, that kind of consistency is rare. Here, it is embedded into the calendar. For an investor, that transforms what appears to be a simple parking operation into a yield-generating system with highly forecastable cash flows.

What makes this particularly compelling is the fragmented nature of ownership. The majority of parking lots and adjacent storage-type properties in these corridors are controlled by small operators, families, or legacy holders. Pricing is often static, operational systems are minimal, and technology adoption is limited. This creates a gap between what the assets are currently producing and what they are capable of producing under a more disciplined, data-driven approach.

The operational leverage is unusually attractive. Unlike traditional real estate plays that require significant capital expenditure, the path to higher returns here is largely driven by optimization rather than redevelopment. Dynamic pricing models, reservation systems, mobile payments, and demand forecasting can materially increase revenue per space without changing the underlying asset. In effect, software becomes the primary driver of margin expansion.

The same thesis extends naturally into storage yards. Both parking lots and storage assets share core characteristics: fixed or slow-growing supply, inelastic demand tied to real-world use cases, and historically inefficient pricing. Contractors, logistics operators, and small businesses require space in specific locations, often with limited substitutes. As with event parking, the willingness to pay is higher than current pricing structures reflect.

There is also a behavioral layer worth noting. As prices increase, some users will shift to alternatives such as public transit. However, this does not eliminate demand—it stratifies it. Parking closest to the venue evolves into a premium product, purchased by those who value time, convenience, and certainty. This segmentation is critical, as it allows operators to capture higher margins on a subset of users while maintaining overall utilization across the system.

The broader investment thesis is straightforward: acquire and aggregate under-managed parking and storage assets in proximity to high-demand nodes—stadiums, medical centers, transportation hubs—and apply a technology-enabled operating layer that optimizes pricing and utilization. The result is not just incremental income growth, but a re-rating of the asset class itself.

What appears, at first glance, to be a local story about rising parking costs is, in reality, early evidence of a larger shift. These assets—long treated as passive, low-growth real estate—are being revealed as mispriced infrastructure. With the right operational framework, they offer the potential for durable cash flow, strong margins, and scalable returns.

Parking and storage around dense event hubs are starting to look less like passive real estate and more like programmable infrastructure where pricing, software, and demand spikes drive outsized returns